Why Did Artax Die in the Swamp of Sadness?

Something or The Nothing, and other important questions.

I started this morning thinking about "the grind," but to me, that phrase—how I’ve used it in the past—implies the slow, steady, low-volatility grind higher. Then I thought about nothingness, like being in a holding pattern. And, of course, my brain jumped to The Neverending Story and the parasitic force, The Nothing.

The Nothing is a dark force absorbing Fantastica. As hope and joy are lost, more and more of Fantastica gets sucked into oblivion. What’s funny is when the Rockbiter, while comparing The Nothing to a hole, says, “At least a hole would be something. This is nothing.”

Did we accidentally join a book club?

When some people look at the price, they see something. Perhaps they see "a triple top formation." Maybe. Honestly, I have no idea.

I know what it might sound like, but I’m trying my hardest not to say, “That’s an old way of thinking…”

Options are a thing; they can change. Their distribution, their makeup, and their use may change, but not by much.

Is a triple top something or nothing when upward moves that would invalidate it happen more often?

I’m not here to predict the size or direction of any move on any day, but I can measure what has already happened.

This is simply a comparison between two basic measures of the SPX. Imagine the multitude of investment decisions being made in different ways, on different assets.

So, is it something or nothing?

It sure feels like The Neverending Story.

This is the most important FOMC meeting of our lifetime... until the next one.

This is the most important presidential election ever... until the next one.

The Fed balance sheet is the only way to measure the economy... until it isn’t.

Janet Yellen is the Wizard of Oz behind the curtain... until she isn’t.

The BoJ is now the real Wizard of Oz; we were just joking about Janet.

Jensen Huang is really the true Wizard of Oz. We weren’t wrong. You were wrong. We know exactly what’s going on here.

Bad wizard doing weird balance sheet things with the Magnificent 7 competitors.

Look at the Magnificent 7—they’re up.

No, no, look over here, not at the Magnificent 7, because they’re down today.

Up.

Down.

Bonds.

November FOMC is the most important thing ever in the history of PPI. Wait... what are we doing today?

Its a full moon and I’m on tilt. Go read this instead.

Navigating Recency Bias and Volatility with a Steady Hand

Recency bias is an interesting phenomenon.

You shouldn’t come here for answers; if nothing else, I only hope you leave with better questions.

Daily

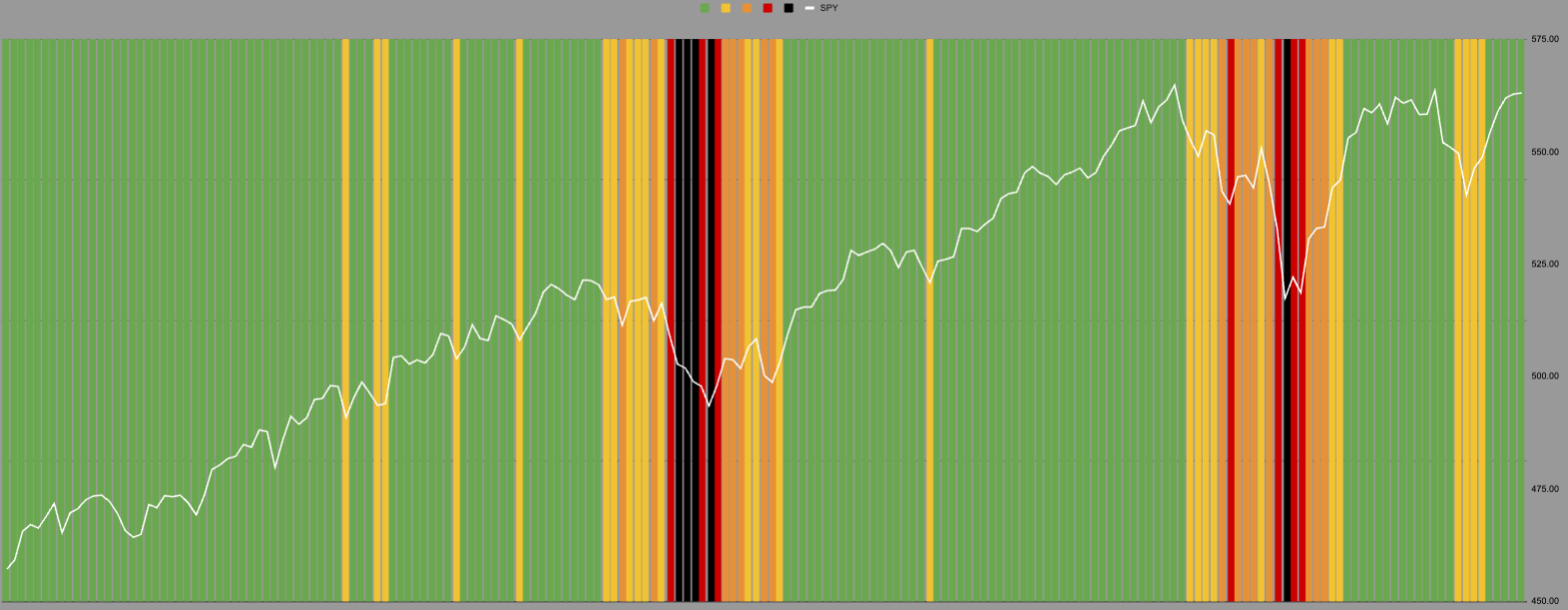

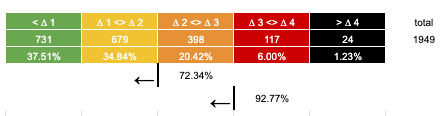

When we take these rainbow charts—I don’t have a better way to describe them—they’re colored using downside measures.

If we take the same measures (sorry, no chart) of the upside, we’re currently in yellow. When you look at the distribution, we are more likely to see upward moves if we’ve already seen upward moves.

This is the metaphor: markets go up the escalator and down the elevator.

Why did I link the post above?

Without getting too wonky, we have to balance the game as we move forward against people who are trying not to lose the last game they just lost.

In July, no one was talking about equity risks. In fact, I received more than one question about why my portfolio positions were only 2%, and whether we could see better returns with larger positions.

Everyone right now is worried about slowing growth. Does 50bps mean the Fed knows something? Was the VIX spike just a pre-tremor?

Who knows, right?

Going back to 2016, there’s a 20% chance we see an upward move, however short-lived, into the orange zone.

Take from this what you will.

Remember, I can think this way because my portfolio currently allows it. I haven’t experienced any major drawdowns this year, but that doesn’t mean it won’t happen. Though I’m fully allocated, I know where—barring gap risk—I’ll reduce or close positions.

I’m not reliant on getting a day move right to define my returns or being right or wrong.

Now I’m going to go cry for Artax.

RIP.