Is the SPX a BUY again?

Maybe, with defined risk and timeframes..

I have said this before: THE MARKET DEFINES WHAT NEWS IS IMPORTANT!

Although the SPX is lower, it is not crashing, which means any news from the last four days is not significant.

I am not trying to diminish the importance of real-world events, but I want to put into perspective the nonsense propagated by the financial media, including all our favourite Twitter celebrities.

The need for attention and clicks means the pull is strong to write about calamity after calamity. I know because some of my favourite posts come when the market is calm, because I have the space to think. When the market is calm the number of readers falls, so some of my best work is read by the fewest people.

Can the SPX fall further from here?

Yes. Volatility is above trend, which is negative for the index. The index itself is below trend and also in negative momentum.

Can the SPX rise from here?

Yes.

If we move down in timeframe from daily to hourly data, we can see some constructive signs.

The equivalent of our 1m and 3m measures on the daily chart have bottomed out on the hourly chart.

We are now above hourly momentum, and the combined signal strength measure is at a very low level. Additionally, we have a combination of triggers that, in the past, have been constructive.

Using our levels viewed through a simpler lens, I hope to convey that the price itself is not the most important factor in the decision-making process.

Where the price is within the levels is far more critical.

Let’s put this in the context of “paying up,” i.e., buying something at a higher price. Buying something at 540 that you could have bought at 530 or 520 is the correct thing to do when viewed through a risk management process.

There are two scenarios to consider:

You didn’t sell the asset you're trying to buy again at a lower price, compounding your layers of risk. What if the dip isn’t a dip?

You sold some or all of the assets you're trying to buy, allowing yourself room to manage your exposure.

These are not the same. What I am referring to is scenario 2. We managed our exposure; we de-risked either directly at the index level or via our portfolio.

The last domino fell in my favour, which gave me room to be clear and thoughtful about my next move.

I don’t have to rush. I am not acting out of fear or greed. I don’t have to do anything.

So what am I doing?

I am using the space I created for myself over the last four weeks, combined with everything mentioned above, to start buying calls.

This is a very small move. At the short timeframe, I can be constructive, knowing that one layer above, at the daily level, still shows weakness. This immediately restricts the level of risk and exposure I want to take.

We have the data, so we should use it.

A move to bullish on the daily measure cannot happen without first happening on the hourly. Only when everything aligns do we increase our exposure.

Think of it like two individual systems (which it is) when I trade futures.

Let’s say my max portfolio exposure at this time can be 2% in SP futures. The hourly system allows me to be at 1%, i.e., 50% of total exposure. Only when the daily agrees can I reach my maximum exposure.

This also works in reverse. The short-term hourly system will make me reduce my exposure from the max earlier than the daily. The daily may not shift at all, and all we have is a small loop within a larger loop.

This could be a very limited short-term loop that I may or may not profit from, while the daily continues to lead the way lower.

This is why I am using calls in a much smaller size.

I hope this helps.

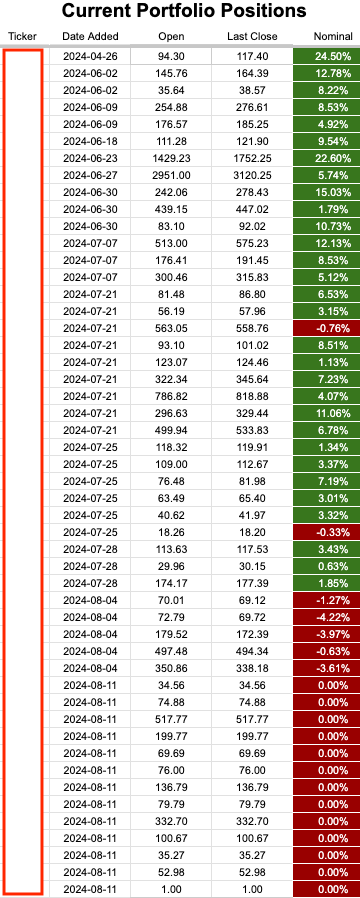

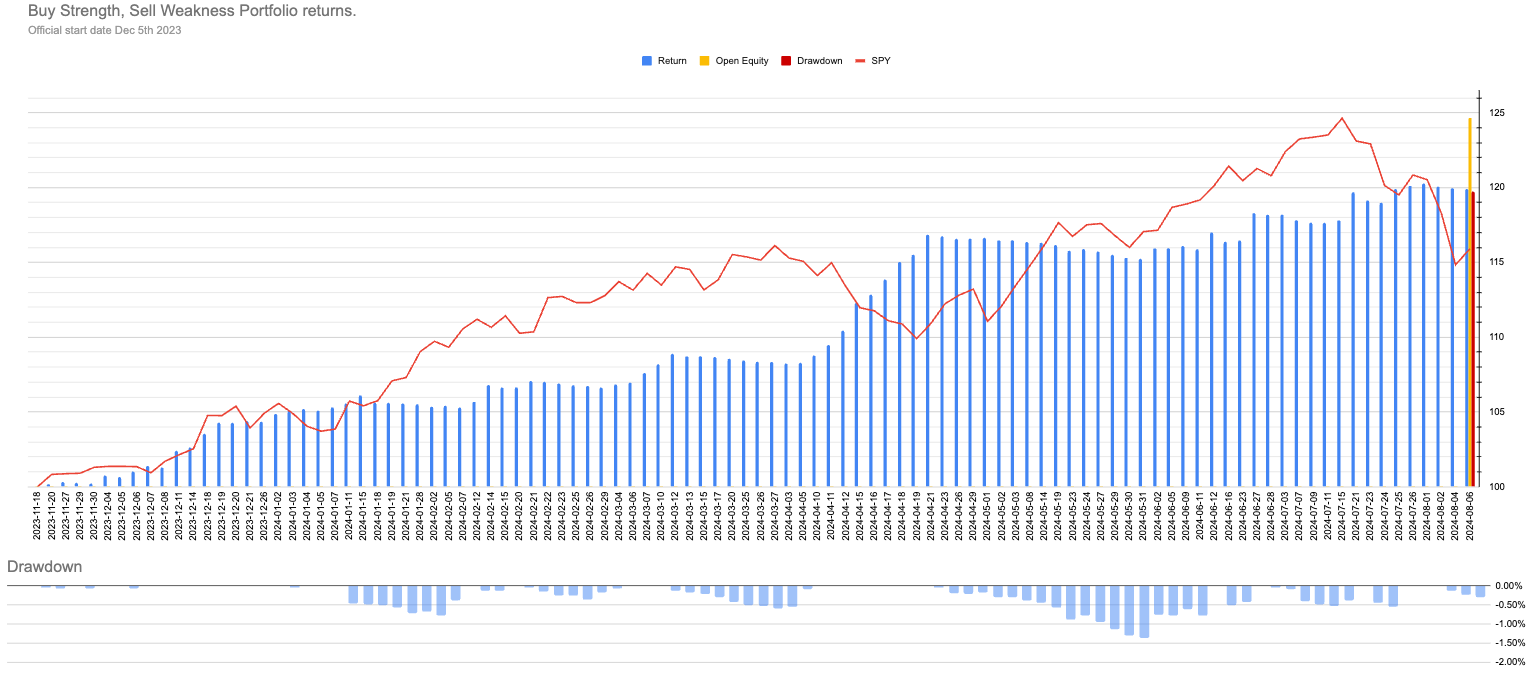

Separate from this detail at the index level, we also dive into the internals and build a portfolio of the current companies with momentum.

Despite the index selling off, we still have many double-digit returns in the portfolio.

We made the shift to sell technology and increase our overweight to utilities and staples almost a month ago.

The discussion for us—again, not driven by fear—is how we manage a potential shift from safety to risk again.

Performance:

Current closed equity return = 19.9%

Current open equity return = 24.7%

If all current positions close at stops, our return = 20%

Using the same measures I discussed for the SPX, we have defined risk and stop losses. With our current open positions, we are just below a 25% return since starting this journey last November.

With the safety hat on, barring any huge gap event, our closed equity return will be around 20%.