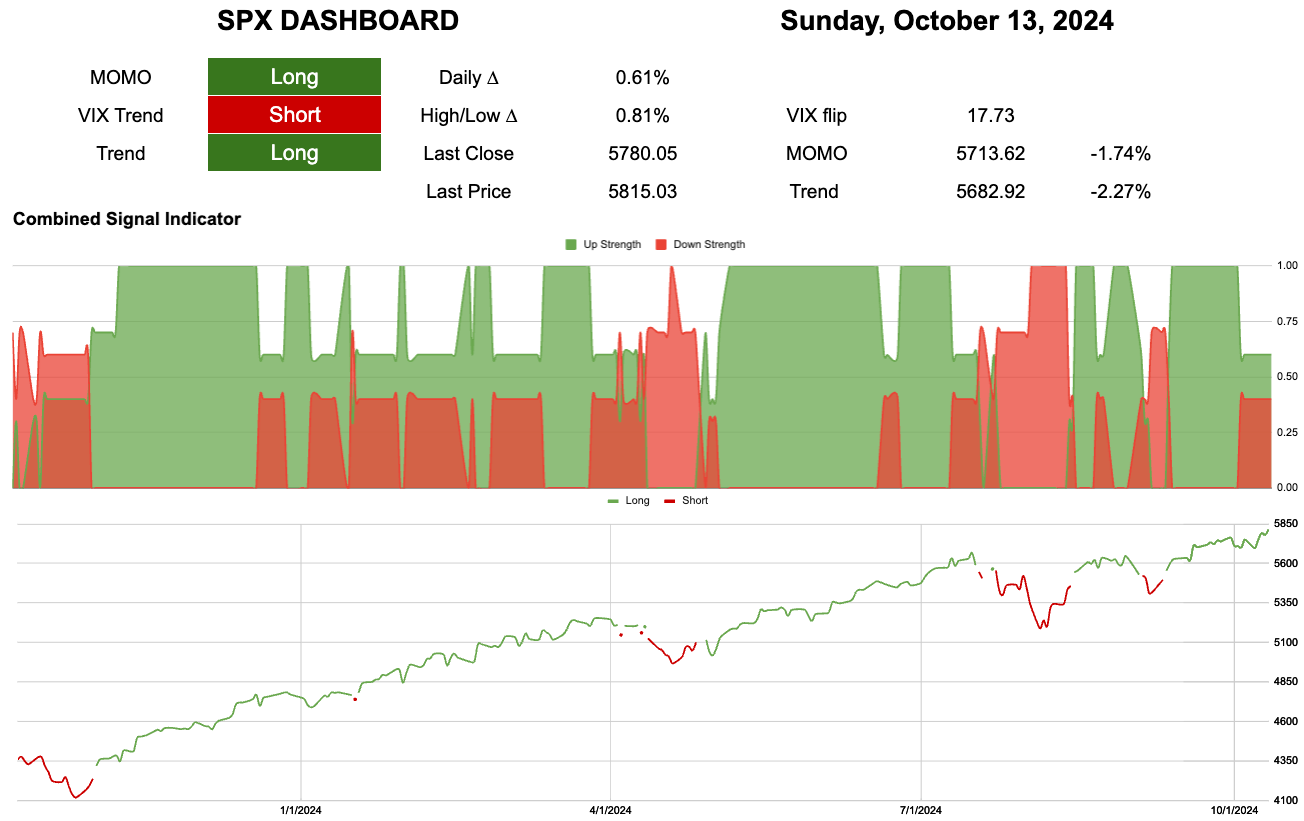

Implied Vs Realised. Options Vs Trend.

The 5682-5713 range marks a critical threshold.

There's plenty of "implied" volatility to consider through the VIX complex, while realized volatility continues to fall. This highlights the disparity between options strategies and trend strategies. Buying calls can be expensive due to high implied volatility, suggesting that trend followers may be in control. As realized volatility decreases, their equity longs can increase.

You can observe the ongoing shift from a risk-off to a risk-on environment over the past month or so.

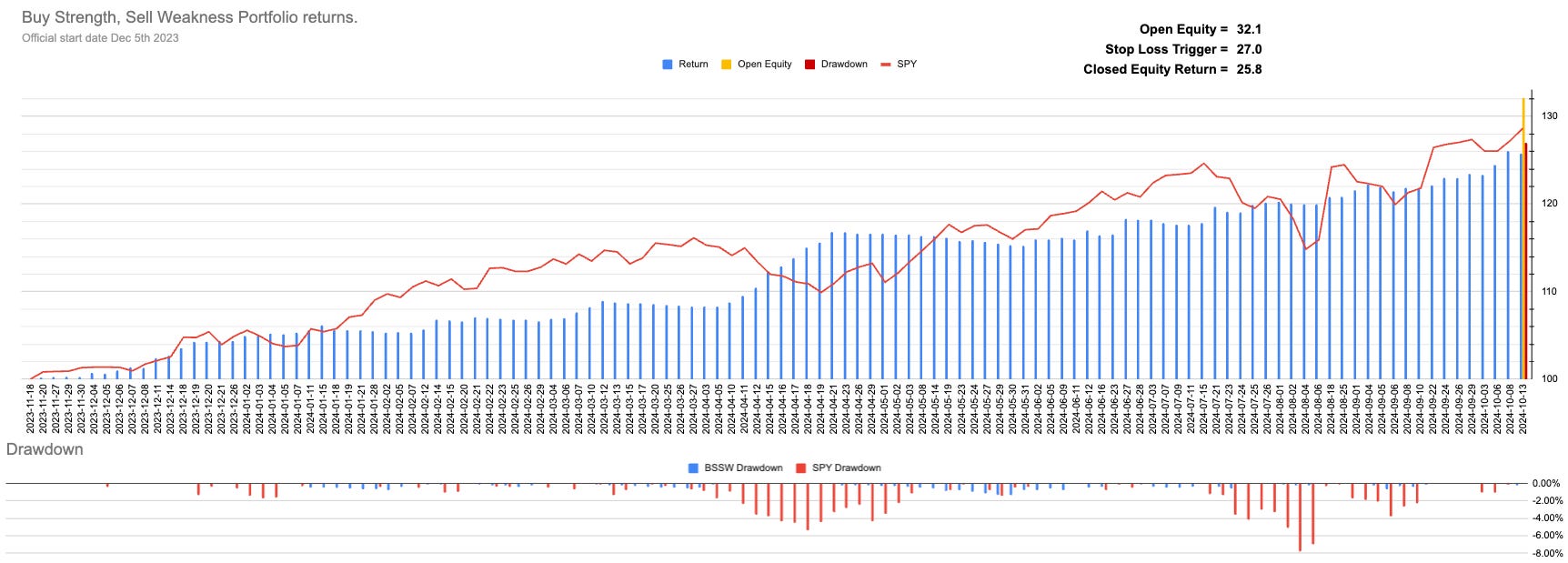

Below, you can see our performance relative to the S&P 500.

"Seems like a lot of work just to match the benchmark."

Yes, and it is, to an extent. However, if you look at the bottom section of the chart, you may not notice it clearly because the SPY had a drawdown of -8% from its previous high in August, while our portfolio drawdown was less than -2%.

Since November 2022, you might wonder why we bother—and after two years, you might be right to question it. But we need to remember that the rest of 2022 happened. So did 2020 and 2018. What if we could mitigate those drawdowns and position ourselves better to capture the upside?

That is what the extra work is for.

Current Closed Equity Return = 25.8%

Current Open Equity = 32.1%

Stop Loss Trigger = 25.8%

Here is an example of the positions that we have closed this week.